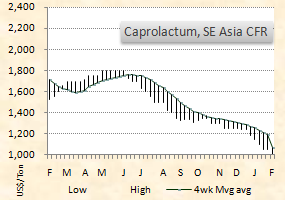

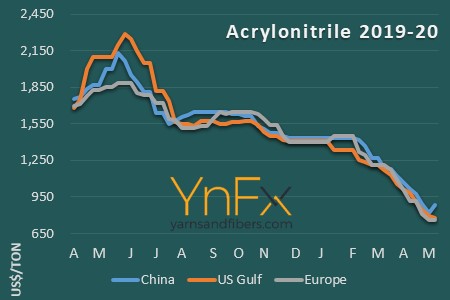

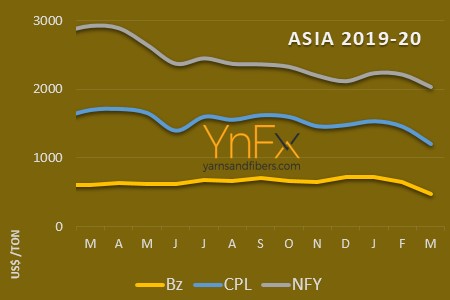

Caprolactum market sees decent demand

YarnsandFibers News Bureau 2016-04-26 10:38:28 –In China, liquid good offers were stable in the second week of April while solid goods offers fell US$30 a ton on the week.

Asian markers, the SE and FE markers gained US$10-20 a ton during the week.

Sinopec retained April contract for liquid goods while Fibrant (formerly DSM Nanjing) kept April nomination unchanged for liquid goods.

Caprolactum prices moved sideways that week on decent demand and recovering feedstock. Liquid caprolactum offers in spot market in China were quoted at a roll over while mainstream values for low?end solid goods were down. Prices for East European and Japanese goods were up on the week.

Downstream run rates at polymerization units were up and inventory level also rose to 6 days’ worth. Run rates at yarn makers were at closer to 80%, with inventory 26 days’ worth.

Courtesy: Weekly PriceWatch Report

related insights

Market Intelligence

Ask for free sample Report

experience

Customer Base

dedicated team

Countries Served Worldwide

newsletter

Register below to receive our newsletters with latest industry trends and news!